Oct 7, 2022 4:21:00 PM

Weekly Market Wrap 07/10/2022

US jobs data on Friday came in stronger than expected, boosting investor expectations of yet another large rate hike by the Federal Reserve in November. OPEC+ ignored Joe Biden’s request and voted to cut production ahead of the winter months. The UK government made its first major U-turn under Liz Truss’ leadership. Eurozone and German retail sales data fell significantly, as consumer prepare for the expected difficult months ahead as inflation continues to accelerate higher. Credit Suisse looks to calm investors’ concerns after widespread criticism caused concerns over the company’s financial health.

US Markets

The S&P 500 is currently ending the week up 4.43% at 3,744 and the NASDAQ is up 2.02% at 10,788. US Markets opened lower on Friday after higher than expected nonfarm payrolls data and lower than expected unemployment data. Unemployment fell to 3.5%, whilst estimates had predicted the rate to remain unchanged at 3.7%. 263,000 jobs were added in September, slightly ahead of the 250,000 estimate. This jobs data signaled strength in the US economy and reinforced the Federal Reserve’s case for another large rate hike in the November meeting. Markets are currently pricing in a 75bps hike for next month. Investors are now looking ahead to US CPI data which will be released next Thursday, where a small decrease in the rate of inflation is expected.

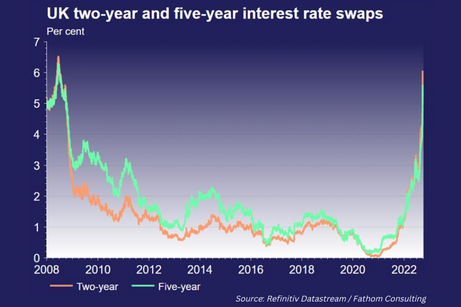

UK Market

The UK market ended the week higher. The UK government remained in the spotlight this week, choosing to reverse the proposed move to abolish the 45p tax rate for the country’s highest earners. The decision was taken after major backlash from both the public and politicians who felt the decision was out of touch with the current climate. UK house prices fell for the second time in the previous three months as rising interest rates are pushing borrowing costs significantly higher for home buyers. It is expected that ongoing higher rates, paired with the cost of living crisis in the UK is expected to reduce demand for homes going forward and see prices continue to push lower, despite the recent government stamp duty cuts.

European Markets

The Euro Stoxx 50 is currently up 2.11% to 3,388, the DAX is up 1.81% at 12,331 whilst the CAC 40 gained 2.09%, reaching 5,882. Data released on Thursday revealed that European retail sales fell by more than expected in August, reinforcing the view that consumer demand is weakening, and public expectations of their future finances is negative. Additional data on Thursday showed that German retail sales had fallen to the lowest level seen in the last 5 years, with food sales falling 1.7% MoM as concerned consumers made efforts to cut back.

Credit Suisse has responded to criticisms of the company’s financial strength by offering to buy back $3billion worth of its own debt in an attempt to reassure investors. European Union leaders are leaning towards proposing a cap on gas prices for the winter ahead, however there have been disagreements over specifics and a number of countries including Germany oppose a cap due to potential difficulties this would cause for the country to buy the gas it requires.

Fixed Income

Yields on the US 10-Year rose slightly to 3.88%, as a number Federal Reserve officials reinforced the message that interest rates are likely to be raised above 4% and be held at that level through most or all of 2023.

Commodities

Brent Crude gained 10.78% this week, as OPEC+ decided to cut oil production by 2 million barrels per day, despite recent calls from US government officials to keep production flowing throughout the winter months.

The Week Ahead

Monday – IMF Meeting

Tuesday – UK Average Earnings

Wednesday – FOMC Minutes

Thursday – US CPI

Friday – US Retail Sales, China CPI

*Price changes as of last week’s close unless stated otherwise.